I have referenced my mother’s influence on my Personal Finance journey many times. Our own children are currently 17 and 11. They are not very interested in financial planning, and I get the “glazed over” look fairly often. However, we cannot give up just because it isn’t easy. 🙂

Before you speak, listen. Before you write, think. Before you spend, earn. Before you invest, investigate. Before you criticize, wait. Before you pray, forgive. Before you quit, try. Before you retire, save. Before you die, give.

WILLIAM A. WARD

This quote summarizes some important life lessons we want our children to follow. They are not all directly related to personal finance, but they cultivate important qualities: patience, perseverance, generosity, and thoughtfulness. We are fortunate that we have financial stability and will try to instill best practices in our kids, but also plan to help them directly. When I was younger I decided I would follow the personal finance guidelines I discussed with my mother, and even if I did not achieve comfortable wealth, I would be able to help my children do so.

I was chatting with my brother-in-law the other day, and he had recently opened a Roth IRA for his daughter. My daughter and her cousin are both 17, only a few months apart. I realized that my daughter had started a part-time job last year, so she had income. Having income is a pre-requisite to opening an IRA account, so we need to follow our own advice and help our daughter start saving for retirement as well. She is still young, but some general advice is to “save as much as you can, as soon as you can, for as long as you can.“

My mother had opened a traditional IRA for me when I was in high school as well. Her mother had left each grandchild $2,000 as inheritance. I worked a lot more hours than my daughter, so I was able to contribute the full amount. Even back then I was maxing out my IRA!

For my daughter, she only made a few hundred dollars, so that will limit her eligible contribution, which can be up to $6,000 for 2021 ($7,000 if 50 or older), but cannot exceed total income. Despite the small amount, this will be an opportunity to experience the power of compound interest first-hand, so hopefully it inspires her own personal finance journey.

My brother-in-law selected a Fidelity Freedom Fund, which is a set of funds that are designed to adjust the investments over time, based on a “target date” for retirement. Since his daughter is 17, he selected 2060 as an initial target. My wife has part of her 401k in one of these accounts, but with a target date of 2030. It is a nice package to provide simplicity, diversification, and risk management.

My usual advice for low maintenance investments would be to buy an S&P 500 Index fund. This was my approach initially, but over time I evolved to be almost 100% invested in individual stocks, bonds, CEFs, ETFs, etc. Per conventional wisdom, I was much more aggressive when I was younger, and pursued more capital gains. Over time, this evolved to building income through dividends and interest, but also managing capital preservation.

Now in July 2021, we are probably in the tail end of a long bull market, with the anomaly of the 2020 bear and bull market thrown in. I feel like the S&P and other indexes are probably getting a little “frothy” or overvalued. We will have discussions with my daughter on her own plan, maybe we can come up with some individual stocks based on her own experience and preferences.

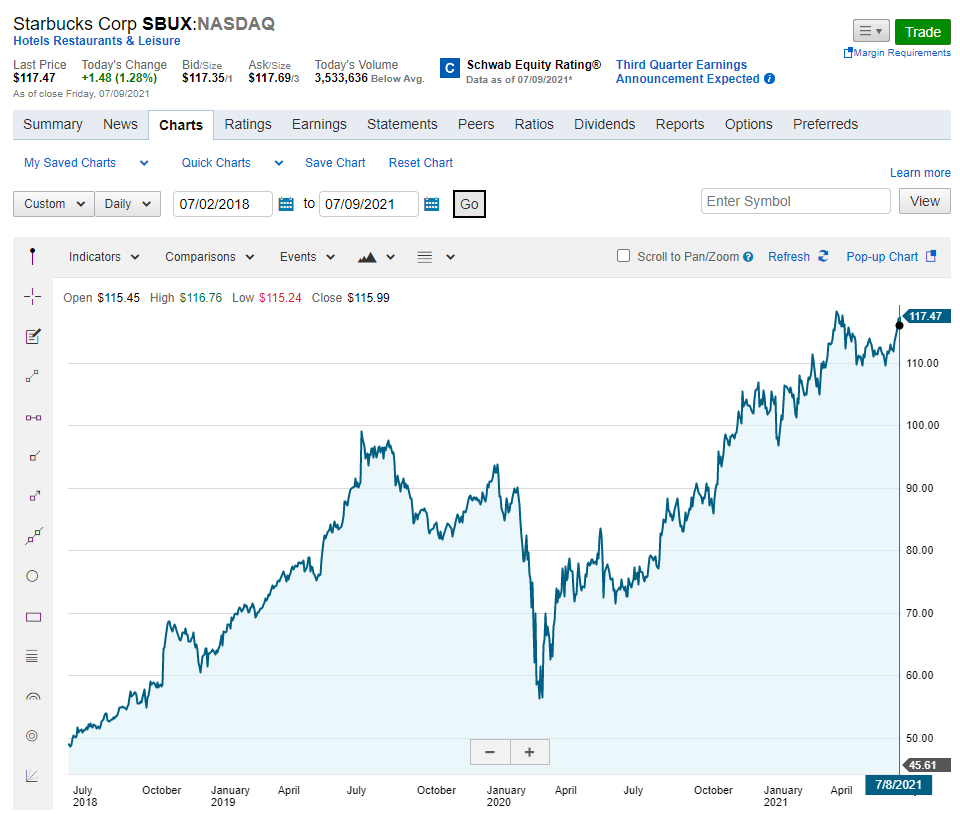

Years ago, we had a retirement seminar through my employer, and the presenter suggested buying “what you know“. For example, if you get a coffee at Starbucks (SBUX-Nasdaq) every day, and notice that it’s always packed, maybe that would be a good investment? We bought some in July 2018 @ $48.88, so it has done well for us. The dividend yield is currently only 1.57%, due to capital appreciation it has gone down, so we may trim to reallocate to something that provides more income.

Subscribe to get email updates when we post new content and please discuss further in the comments below or let me know if you have any questions or other feedback.

| Disclaimer: I am not a financial planner and content on this site is meant to provide food for thought, not professional advice. I share my experiences to show what worked so far and what didn’t, YMMV. Please consult your financial advisor or tax professional as needed. |